AI is actually helping Atlassian’s business

Wall Street thought AI was a threat to software companies for two reasons. First, analysts thought tools such as Anthropic’s Claude Code would allow businesses to develop their own versions of products such as Jira and Confluence, making companies Atlassian redundant. Second, if AI resulted in widespread job losses, the Street felt software companies with seat-based revenue models would lose a chunk of their income.

To counter the first issue, Atlassian doesn’t just sell software. It provides the security, infrastructure, and technical support required to deploy Jira and Confluence successfully. These things cost a ton of money to set up and maintain, which is only profitable at scale. In other words, the average business might be able to clone Jira and Confluence using an AI coding assistant, but preventing data breaches and maintaining uptime is a whole other challenge.

Plus, Atlassian developed its own AI platform called Rovo, which comes with an entire suite of features to enhance the capabilities of Jira and Confluence. It includes an advanced search tool that can instantly locate information from across the organization, even if it isn’t stored within the Atlassian ecosystem. Rovo can also serve as a coding assistant to help software developers accelerate their workflows, which is the ultimate addition to a product Jira.

More than 350,000 businesses worldwide use Atlassian, so the company has a treasure trove of data with which to improve its AI models. This advantage makes Rovo more useful than most generic AI assistants, which further entrenches the Atlassian software ecosystem deeper into each organization.

Now, on to Wall Street’s second concern.

A surprise acceleration in revenue growth

Atlassian generated $1.8 billion in total revenue during its fiscal 2026 third quarter (ended March 31), which blew away Wall Street’s estimate of $1.7 billion. It was a 32% increase from the year-ago period, marking a sharp acceleration from the 23% growth the company delivered three months earlier in the second quarter. That alone squashed concerns that AI was causing a loss in revenue for software companies.

In fact, Atlassian said annual recurring revenue (ARR) from Rovo customers grew at twice the pace of ARR from non-Rovo customers. So, again, AI is proving to be a massive tailwind for this company, not a threat.

Expand

NASDAQ: TEAM

Atlassian

Today’s Change

(15.48%) $14.44

Current Price

$107.73

Key Data Points

Market Cap

$27B

Day’s Range

$97.44 – $108.48

52wk Range

$56.01 – $222.59

Volume

13.9K

Avg Vol

7.4M

Gross Margin

84.50%

To ease concerns even further, Atlassian launched a new pricing option for customers on May 6. It’s called Flex, and it allows enterprises to set a budget they can allocate to any Atlassian products during their contract period, without having to negotiate new terms. The company calls it a value-based pricing model, because customers are paying based on what they use, not how many seats, or users, they might have within a specific time frame.

Flex will make it significantly easier for new customers to get up and running with Atlassian, which could drive further momentum at the top line. Cybersecurity giant CrowdStrike launched a similar flexible subscription option in 2023, and it continues to fuel an acceleration in the company’s revenue growth to this day.

Why Atlassian still has room to run

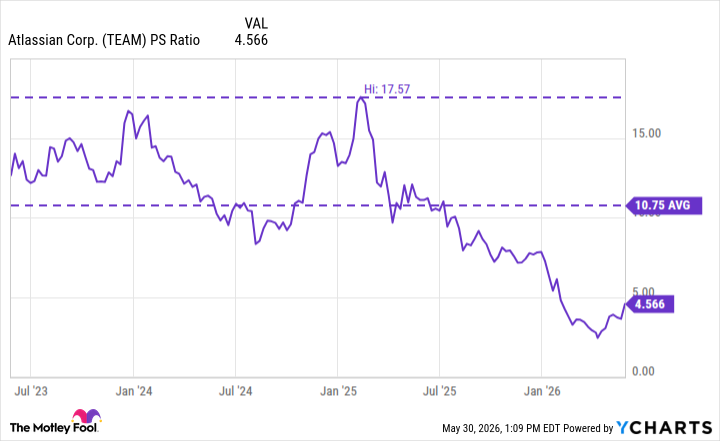

Despite the blistering gains in Atlassian stock since April, it’s still trading at a price-to-sales (P/S) ratio of just 4.5 — far below its three-year average of 10.7, and even further below last year’s peak of 17.5.

TEAM PS Ratio data by YCharts

Atlassian stock would have to soar by 137% from last Friday’s close just to match its three-year average P/S ratio, which I think is entirely possible considering the company’s accelerating revenue growth. That would result in a stock price of $255.

But I intend to hold the stock beyond that point, because I think the company is entering an era of faster growth and innovation as it capitalizes on the AI opportunity over the next few years.

Read Next

![]()

•By Adam Levy

1 Software Stock to Buy Before It Doubles, According to Select Analysts

•By Anthony Di Pizio

I Bought Atlassian Stock When It Was Down 87%, and Now It’s Soaring. These Were My Reasons.

![]()

•By Adam Spatacco

Beyond Hyperscalers: Why Leopold Aschenbrenner Just Bought 5.6% of Nebius

•By Will Ebiefung

Is Palantir Still a Millionaire-Maker Stock?

•By Keithen Drury

3 Reasons Why Now is the Perfect Time to Buy Nvidia Stock

•By Keithen Drury

3 Reasons Why IonQ Is the Best Quantum Computing Pure Play

About the Author

Anthony Di Pizio is a contributing Motley Fool technology analyst covering artificial intelligence, cloud computing, autonomous vehicles, and enterprise software. Previously, Anthony was a licensed fund manager, stock broker, and corporate advisor. He holds a bachelor’s degree in commerce and economics from Macquarie University in Sydney, Australia, along with ASIC RG146 certifications in financial securities and derivatives.

Stocks Mentioned

Atlassian

NASDAQ: TEAM

$107.73

(+15.48%)+$14.44

![]()

Motley Fool Stock Advisor’s Latest Pick

—% Avg Return

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Sumber Artikel:

Fool.com