1. Alphabet is a balanced company at an impeccable valuation

As of 2025, Alphabet owns a little more than 6% of SpaceX, as Alphabet’s initial investment has increased several-fold since 2015. What’s more, Alphabet-owned Google is reportedly paying $920 million per month to lease artificial intelligence (AI) compute capacity from SpaceX over a three-year period. But the two companies are also competitors. Alphabet’s Gemini family of large language models competes with xAI’s Grok, which is owned by SpaceX.

SpaceX has been on a torrid run since going public, but Alphabet is the better all-around buy. Alphabet generated $160.2 billion in trailing 12-month net income — putting it just ahead of Nvidia as the most profitable company in the world. Alphabet’s success with Gemini and its integration of AI features into Google Search and the Google Pixel prove it could continue to play a leading role in the age of AI. Alphabet’s custom-designed chips are driving cost savings and efficiency improvements across its cloud computing infrastructure — namely, Google Cloud.

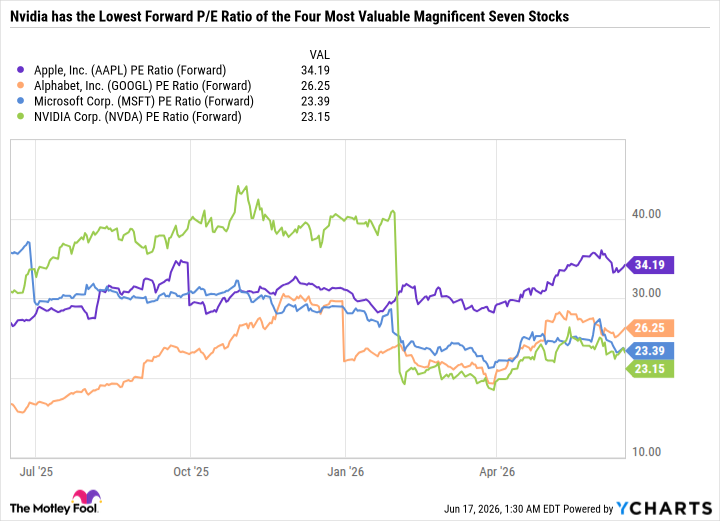

Among the world’s most valuable companies, Alphabet is by far the most diversified yet continues to grow rapidly. And at a mere 26.3 forward price-to-earnings (P/E) ratio, Alphabet is also compellingly valued.

Expand

NASDAQ: SPCX

Space Exploration Technologies

Today’s Change

(-3.44%) $-6.59

Current Price

$185.23

Key Data Points

Market Cap

$2.4T

Day’s Range

$172.11 – $190.00

52wk Range

$149.34 – $225.64

Volume

6.8M

Avg Vol

314.9M

2. SpaceX’s golden opportunity benefits Nvidia

Google and Anthropic are renting compute capacity from SpaceX, some of which involves clusters of Nvidia graphics processing units (GPUs). But SpaceX plans to take its data centers to the stars with orbital AI compute clusters. In fact, building data centers in space could be the core argument for why Elon Musk is targeting $1 trillion in SpaceX revenue by 2031.

In its Form S-1 filing with the Securities and Exchange Commission, SpaceX said it could begin deploying orbital AI compute satellites as early as 2028. Launching these data centers will ly come with a ton of up-front costs, but if SpaceX can fine-tune the process for servicing those data centers (either in space or by bringing them back to the Earth’s surface), then it could pay off in the long run. These closed-loop systems won’t require water-insensitive cooling. And they’ll benefit from free, 24/7 solar power by maintaining a constant position to the sun through sun-synchronous orbit.

Nvidia would love nothing more than millions of data centers orbiting Earth chock-full of Nvidia GPUs and networking chips. Not only could SpaceX become a key customer, but it would ly want to outfit its data centers with the most cutting-edge chips available, given the maintenance challenges of servicing low-Earth orbit satellites. That makes SpaceX a large potential buyer for AI hardware, and no company is better positioned to develop rack-scale AI solutions than Nvidia. Best of all, Nvidia is even cheaper than Alphabet, with a forward P/E ratio of just 23.2.

AAPL PE Ratio (Forward) data by YCharts

3. Microsoft has fallen far enough

Down 22% year to date, Microsoft is by far the worst-performing Magnificent Seven stock in 2026. But the sell-off could be a buying opportunity for long-term investors.

Although SpaceX’s investment thesis is built entirely on its anticipated growth potential, Microsoft has become an out-of-favor dividend-paying value stock. Microsoft has fallen behind Amazon and Alphabet in designing its own AI chips. Microsoft has also been a longtime backer of OpenAI and powers Microsoft Copilot with OpenAI’s models. But Copilot’s effectiveness has faced scrutiny, and OpenAI’s ChatGPT isn’t growing as quickly as Anthropic’s Claude. What’s more, the software industry is under intense pressure from AI, which puts the Microsoft 365 software suite in the crosshairs.

The knee-jerk narrative may be that Microsoft is being disrupted while companies SpaceX are doing the disrupting. And while Microsoft certainly hasn’t executed to perfection in recent quarters, it’s a mistake to assume its best days are behind it.

Microsoft continues to deliver high-margin earnings growth and maintains a rock-solid balance sheet. Microsoft Azure benefits from AI compute needs. And given how entrenched Microsoft’s software is in enterprise and everyday use cases, it’s doubtful that it faces nearly the disruption risk as other software products.

4. Apple is patient for all the right reasons

Apple has gotten a lot of flak for its lack of AI spending, choosing instead to generate gobs of free cash flow and buy back more stock than any other U.S. company. Meanwhile, Amazon will ly go free cash flow negative in 2026, Alphabet just raised $85 billion to fund its AI spending, and Meta Platforms and Microsoft continue to ramp up spending.

But Apple’s focus on cash flow makes sense given its consumer-facing nature. Rolling out technologically advanced features and products means little if they aren’t user-friendly and privacy-protected. Trust is a cornerstone of Apple’s business model, as a single customer can use multiple high-margin products and services.

However, Apple is more expensive based on forward earnings than Nvidia, Microsoft, and other companies. It could also continue increasing earnings at the slowest rate of these companies, making it more of a stable stalwart tech stock than a high-growth engine.

Even so, I’d still rather buy Apple than SpaceX, at least until SpaceX bridges the gap between expectations and reality. Apple’s history is chock-full of new product releases that were slow to catch on at first but then became smash hits — the Apple Watch. If any company is going to roll out a consumer-friendly AI-powered tech product, it’s Apple, and if it does, that could change the narrative and help justify its premium valuation.

Read Next

•By Ryan Vanzo

This SpaceX Catalyst Is Coming. Here’s Why Smart Investors Are Buying Before August.

•By Adria Cimino

Here’s What I Think Is Going on With SpaceX Stock

![]()

•By Jeremy Bowman

Best IPO Stocks to Buy in 2026: Latest Upcoming Stocks to Watch

•By Stefon Walters

•By Adam Levy

Should You Buy SpaceX Stock After Its IPO Pop? History Offers a Clear Answer.

•By Chris Neiger

Does a SpaceX and Tesla Merger Make Sense? Here’s What Investors Should Know

About the Author

Daniel Foelber is a contributing Motley Fool stock market analyst with extensive experience covering the broader stock market and publicly traded companies across energy, industrials, utilities, materials, technology, communications, consumer discretionary, consumer staples, and financial stocks. Daniel looks for industry leaders offering compelling growth, value, or dividends to generate passive income. He has also written for energy trade publications and helped build oil and gas training modules. He holds a bachelor’s degree in finance and a certificate in personal financial planning from the University of Houston. He believes the best investors are those who focus on fundamentals, remain steady through volatility, and filter out market noise.

Stocks Mentioned

Space Exploration Technologies

NASDAQ: SPCX

$185.23

(-3.44%)-$6.59

![]()

Motley Fool Stock Advisor’s Latest Pick

—% Avg Return

Apple

NASDAQ: AAPL

$298.01

(+0.70%)+$2.06

Microsoft

NASDAQ: MSFT

$379.62

(+0.19%)+$0.71

Alphabet

NASDAQ: GOOGL

$368.49

(+1.29%)+$4.70

Nvidia

NASDAQ: NVDA

$210.95

(+3.08%)+$6.30

Meta Platforms

NASDAQ: META

$578.16

(+1.86%)+$10.58

Tesla

NASDAQ: TSLA

$401.06

(+1.18%)+$4.68

Amazon

NASDAQ: AMZN

$244.65

(+3.01%)+$7.15

Alphabet

NASDAQ: GOOG

$367.82

(+1.58%)+$5.72

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Sumber Artikel:

Fool.com