By James Halley – Mar 7, 2026 at 5:55AM EST

Key Points

-

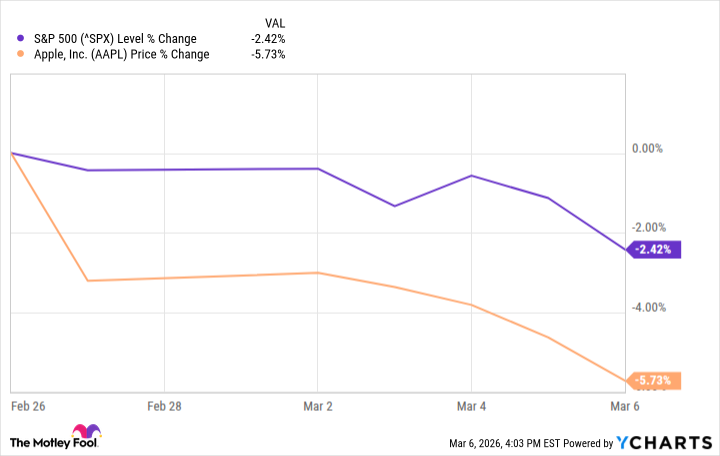

Apple s have slid by more than 5% since the Iran War began.

-

After an initial rise on Monday, Williams Companies s have dropped.

-

Both companies have solid financials and plenty of cash to help them weather any periods of economic turmoil.

Expand

NASDAQ: AAPL

Apple

Today’s Change

(-0.96%) $-2.49

Current Price

$257.80

Key Data Points

Market Cap

$3.8T

Day’s Range

$254.43 – $258.76

52wk Range

$169.21 – $288.62

Volume

1.8M

Avg Vol

48M

Gross Margin

47.33%

Dividend Yield

0.40%

Why Apple is a blue chip stock

Apple, though it has only been a public company since 1980, is the ultimate blue chip stock. With a market cap of $3.85 trillion, it is the second-largest company in the world, behind only Nvidia. It has ample stability, with more than $35.9 billion in cash and short-term investments on its books, giving it enough of a cushion to weather any economic setback. While it is a growth stock, it has shown a commitment to dividend hikes and buybacks. It has raised its dividend for 11 consecutive years, and it repurchased $24.7 billion worth of its stock in the first quarter of its fiscal 2026 alone.

Why Apple’s recent setback is an overreaction

As of the close of trading Friday, Apple stock had fallen by almost 6% since Feb 26, compared to the S&P 500‘s fall of a little over 2.4% in that same period.

Obviously, as a vertically integrated technology lifestyle brand, Apple isn’t that affected by oil prices, though a sustained downturn in the economy would hit its business, as it would nearly any consumer company.

In its fiscal 2026 first quarter, which ended Dec. 27, Apple delivered record revenue of $143.8 billion, up 16% year over year, while earnings per (EPS) grew 19% to a record $2.84.

Apple has been criticized for its weak efforts in the artificial intelligence (AI) race, and particularly for its delays in rolling out AI enhancements to Siri, its virtual assistant. However, some are now thinking the company has been smart to not spend too much yet on AI.

Its flagship product, the iPhone, continues to defy expectations. During Apple’s latest earnings call, CEO Tim Cook said that global demand for the iPhone remained “staggering,” an assertion supported by its 23% year-over-year revenue growth and all-time sales records across every geographic region. Sales of the devices, driven by the successful rollout of the iPhone 17 family, accounted for 59% of Apple’s total revenue.

The company is also working to expand its customer base by delivering some less-expensive products (at least, by Apple’s standards), including the MacBook Neo, and the iPhone 17e, both of which are priced at $599.

Expand

NYSE: WMB

Williams Companies

Today’s Change

(-0.75%) $-0.56

Current Price

$74.21

Key Data Points

Market Cap

$91B

Day’s Range

$73.94 – $75.11

52wk Range

$51.58 – $76.87

Volume

199K

Avg Vol

7.3M

Gross Margin

41.57%

Dividend Yield

2.69%

Why Williams Companies is a blue chip stock

Though its market cap of $93 billion makes it far smaller than Apple, Williams Companies has a much deeper history, having been founded in 1908. It certainly is a blue chip within the energy and infrastructure sector, and has raised its dividends for eight consecutive years, including a 6% increase this year. At the current price, it has a yield of around 2.7%.

Its natural gas infrastructure gives it stability because it leases its services through long-term, fee-based contracts. This gives it predictable cash flows, and because it is a midstream player, its profits are not particularly sensitive to changing oil prices.

Why its recent pullback is an overreaction

The Williams Companies’ stock, after rising to $76.75 per on Monday, closed at $74.22 on Friday. That 3.3% drop, though small, seems silly considering the company’s long-term strength.

Williams Companies currently handles approximately one-third of the natural gas consumed in the United States. Its 33,000-mile pipeline network operates entirely within domestic borders, providing it with a natural hedge against President Donald Trump’s tariffs. This geographic focus, paired with long-term service contracts, ensures a steady and dependable stream of cash flow that has supported 13 consecutive years of growth in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA).

The company’s 2025 performance was particularly robust, with adjusted EBITDA rising 9% to $7.8 billion and total revenue climbing 13.7% to $11.9 billion. This financial strength translated to a 17.5% increase in EPS to $2.14, while the stock price is up by more than 23% so far this year. Much of this momentum was fueled by the rapid buildout of new data centers, which increasingly rely on natural gas power plants for electricity. Demand was further bolstered by a colder-than-usual winter across the eastern half of the U.S., which drove a significant spike in natural gas consumption for heating.

Williams continues to prioritize holder returns. It has paid out dividends for 52 consecutive years, and its distributions are covered 2.4 times by its adjusted funds from operations. This healthy coverage ratio not only underscores the safety of the current payout but also provides management with significant flexibility for future increases.

Read Next

![]()

The Williams Companies, inc (WMB) Q3 2021 Earnings Call Transcript

![]()

Williams Companies Inc (WMB) Q4 2020 Earnings Call Transcript

![]()

Williams Companies Inc (WMB) Q3 2020 Earnings Call Transcript

![]()

Williams Companies Inc (WMB) Q2 2020 Earnings Call Transcript

![]()

Williams Companies Inc. (WMB) Q3 2018 Earnings Conference Call Transcript

•By Alyce Lomax

When Companies Reap What They Sow: Disaster

Stocks Mentioned

Williams Companies

NYSE: WMB

$74.21

(-0.75%)-$0.56

Apple

NASDAQ: AAPL

$257.80

(-0.96%)-$2.49

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Sumber Artikel:

Fool.com