By Harsh Chauhan – Apr 1, 2026 at 11:00PM EST

Key Points

-

One of the companies discussed in this article produces a key component that will help the Vera Rubin chips reach their full potential.

-

The other company is a key player in the global semiconductor supply chain that Nvidia relies on to manufacture its chips.

![]()

Image source: TSMC.

1. Micron Technology

Nvidia’s Rubin chips are going to pack more memory capacity and higher bandwidth. The chip giant notes that the dynamic random-access memory (DRAM) capacity of the Rubin NVL72 rack-scale server will increase by 2.5 times over the Blackwell NVL72, and it will pack 1.5 times more high-bandwidth memory (HBM). What’s more, the bandwidth of the HBM on Rubin chips will increase by 2.8 times over Blackwell, suggesting that they will be able to move more data at faster speeds in AI servers.

This is great news for Micron Technology (MU +8.96%) investors. The memory specialist has already commenced the high-volume production of HBM for Rubin chip systems, including both GPUs and central processing units. What’s more, Micron is also producing enterprise solid-state drives (SSDs) for the Rubin platform.

Expand

NASDAQ: MU

Micron Technology

Today’s Change

(8.96%) $30.27

Current Price

$368.11

Key Data Points

Market Cap

$415B

Day’s Range

$343.00 – $377.89

52wk Range

$61.54 – $471.34

Volume

3M

Avg Vol

41M

Gross Margin

58.54%

Dividend Yield

0.13%

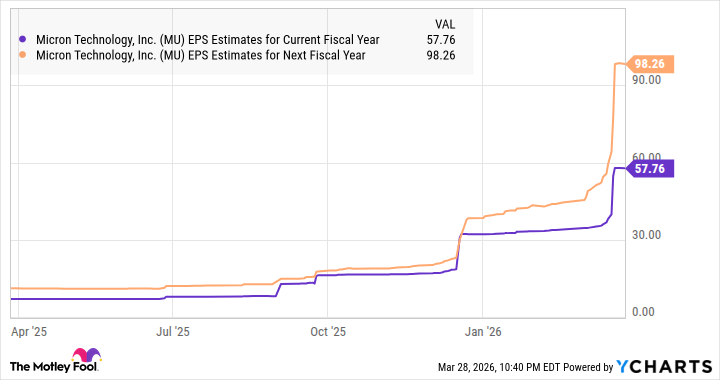

This explains why Micron’s stunning growth is here to stay. The company expects $33.5 billion in revenue in the current quarter, a jump of 260% from the year-ago period. Even better, its earnings are set to jump to $19.15 per in the ongoing quarter from $1.91 per in the same period last year. HBM demand is playing a key role in this phenomenal earnings growth, driving an improvement in Micron’s product mix due to the higher pricing that it commands.

Importantly, Micron’s earnings are expected to grow at exponential rates from the previous fiscal year’s reading of $8.29 per .

MU EPS Estimates for Current Fiscal Year data by YCharts

Micron stock trades at just 20 times earnings right now, presenting investors with a great deal they should consider grabbing with both hands, as it can make them significantly richer in the long run. For instance, this AI stock could jump to $2,260 by the middle of next year if it trades at 23 times earnings at that time (in line with the tech-laden Nasdaq-100 index’s forward earnings multiple), based on the $98.26-per-earnings estimate shown in the chart above.

Micron can therefore jump sixfold from current levels, which is why investors looking to buy a potential growth stock for their million-dollar portfolio should consider buying it.

2. Taiwan Semiconductor Manufacturing

Nvidia relies on its foundry partner, Taiwan Semiconductor Manufacturing (TSM +1.16%), to produce the chips it designs. So, the massive sales forecast for the Blackwell and Rubin chip platforms through next year should ensure solid growth for TSMC, especially considering that it is on track to significantly expand its manufacturing capacity.

Expand

NYSE: TSM

Taiwan Semiconductor Manufacturing

Today’s Change

(1.16%) $3.91

Current Price

$341.86

Key Data Points

Market Cap

$1.8T

Day’s Range

$339.76 – $348.64

52wk Range

$134.25 – $390.20

Volume

701K

Avg Vol

14M

Gross Margin

58.73%

Dividend Yield

0.98%

TSMC has guided for $52 billion to $56 billion in capital expenditures for 2026, up by almost a third over last year’s $40.9 billion at the midpoint. The Taiwan-based company notes it will spend 70% to 80% of its budget on advanced process nodes. Given that the Rubin chips are reportedly going to be produced using TSMC’s advanced 3-nanometer (nm) process node, it is easy to see why TSMC is going to aggressively bring additional capacity online.

Nvidia is TSMC’s largest customer, accounting for 19% of its revenue, according to reports. TSMC reportedly received $23.2 billion in revenue from Nvidia in 2025, more than double the 2024 levels. As TSMC ramps up its production capacity and helps Nvidia fulfill the huge demand for its latest-generation chips, there is a good chance it will outperform Wall Street’s growth expectations.

Consensus estimates project a 36% increase in TSMC’s earnings in 2026 to $14.54 per , ed by a relatively slower 23% increase in 2027 to $17.96 per . However, the $1 trillion in orders Nvidia estimates through the end of next year should be enough for TSMC to clock faster growth.

Assuming TSMC’s earnings jump to even $20 per by the end of 2027 and it trades at 23 times earnings at that time, its stock price could reach $460.

That points to a potential 41% surge in TSMC stock, making the foundry giant an ideal investment for those looking to build a million-dollar portfolio.

Read Next

•By Lyle Daly

The Largest Companies by Market Cap in April 2026

•By Danny Vena, CPA

1 Brilliant Growth Stock to Buy Before It Joins Nvidia, Apple, and Alphabet in the $3 Trillion Club

•By Jack Caporal

The AI Stocks Hedge Funds Love the Most

•By Keithen Drury

1 No-Brainer Semiconductor Stock to Buy With $1,000 Right Now

•By Jeremy Bowman

There Are 10 Trillion-Dollar Stocks On the Market. This Is the Only One That’s Up This Year

About the Author

Harsh Chauhan is a contributing Motley Fool technology analyst covering semiconductors, consumer electronics, artificial intelligence, and software. Harsh previously worked as a journalist for CCN Markets covering crypto and macroeconomics, a contributor at Capital 10x covering metals, mining, and industrial stocks, and a research associate at Zacks Investment Research. He holds a bachelor’s degree in commerce from St. Xavier’s College in Kolkata, India.

Stocks Mentioned

Taiwan Semiconductor Manufacturing

NYSE: TSM

$341.49

(+1.05%)+$3.54

Micron Technology

NASDAQ: MU

$368.11

(+8.96%)+$30.27

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Sumber Artikel:

Fool.com