By Harsh Chauhan – Mar 14, 2026 at 8:05PM EST

Key Points

-

Semiconductors are the basic building blocks powering AI applications across multiple devices.

-

Helping customers integrate AI into their operations can lead to remarkable revenue and earnings growth.

-

Both companies can sustain their healthy growth rates over the next decade, thanks to the secular growth opportunities.

TSMC is the kingpin of AI chips

All kinds of AI hardware, from data centers to smartphones, personal computers, robots, and autonomous cars, need semiconductors to function. After all, the chips used in these applications enable them to perform the calculations required to run AI models and inference solutions. In simple terms, no AI device can function without semiconductors, which are now considered to be the new oil.

Expand

NYSE: TSM

Taiwan Semiconductor Manufacturing

Today’s Change

(0.42%) $1.40

Current Price

$338.11

Key Data Points

Market Cap

$1.8T

Day’s Range

$336.23 – $344.47

52wk Range

$134.25 – $390.20

Volume

562K

Avg Vol

13M

Gross Margin

58.73%

Dividend Yield

0.91%

The proliferation of AI explains why the global semiconductor market’s revenue is projected to more than triple over the next decade to just under $2.8 trillion. TSMC is one of the best semiconductor stocks you can buy to capitalize on this massive opportunity. That’s because the company is the go-to manufacturer of chips that power AI applications.

It manufactures chips for AI data center giants such as Nvidia and Broadcom, for personal computer chip designers such as AMD and Intel, and smartphone-centric players such as Apple, Qualcomm, and MediaTek. It is worth noting that TSMC manufactured chips for a whopping 534 customers last year, producing close to 13,000 products for them across multiple applications.

Not surprisingly, TSMC anticipates its revenue from sales of AI accelerators to clock a compound annual growth rate (CAGR) in the mid-to-high-50% range through 2029. It forecasts its overall revenue to grow at a 25% CAGR over the same period. The long-term opportunity in the semiconductor market should ensure that TSMC sustains its healthy growth over the next decade, especially given that it is the No. 1 foundry manufacturing chips for third parties, with an estimated market of 72%.

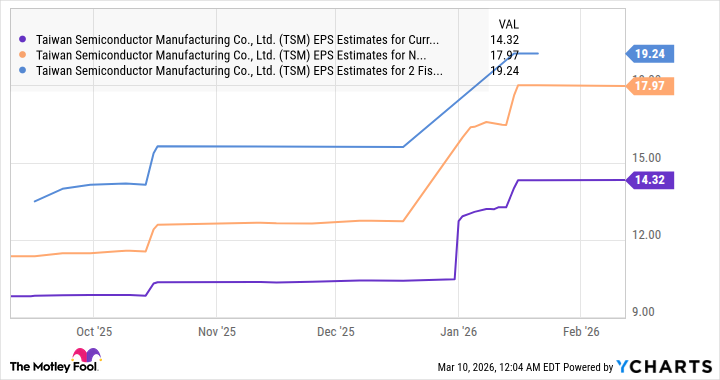

The points discussed above explain why analysts are bullish on TSMC’s prospects and have raised their earnings expectations of late, a trend that should continue in the future as well due to the semiconductor market’s secular growth.

Data by YCharts.

That’s why investors looking to buy an AI stock to buy right now and hold for the long haul should take a closer look at TSMC stock since it trades at an attractive 26 times forward earnings.

Palantir Technologies is helping customers reap the benefits of AI with its software solutions

While TSMC’s hardware provides the basic building blocks that enable AI model training and inference, Palantir provides a software platform that enables end customers to deploy generative AI into their operations. Introduced in April 2023, Palantir’s Artificial Intelligence Platform (AIP) has been a huge success.

Expand

NASDAQ: PLTR

Palantir Technologies

Today’s Change

(-1.66%) $-2.55

Current Price

$150.95

Key Data Points

Market Cap

$361B

Day’s Range

$148.58 – $154.56

52wk Range

$66.12 – $207.52

Volume

42M

Avg Vol

49M

Gross Margin

82.37%

This platform enables customers to integrate their data with large language models to automate processes, improve decision-making with real-time data, and develop AI applications and agents. As a result, Palantir’s customer growth and deal sizes have taken off since the introduction of AIP.

The company ended 2025 with 954 customers, an increase of 34% from the year-ago period. The number of deals worth $1 million or more stood at 180, a massive increase over the 55 such deals it cracked in the final quarter of 2022 (before the introduction of AIP). The number of $10 million-plus deals has shot up 12-fold during this period, clearly indicating that customers are flocking to Palantir thanks to the gains that AIP delivers.

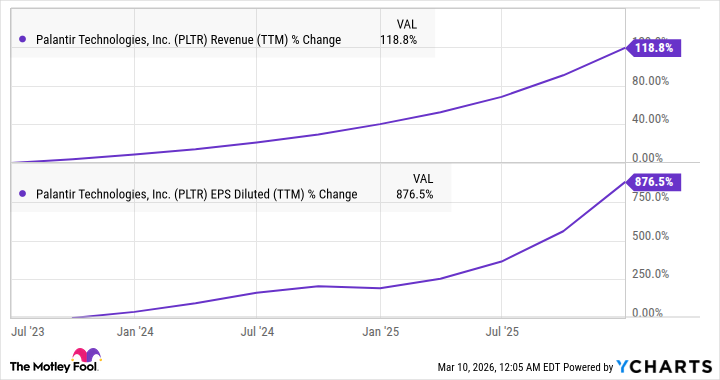

The robust growth in Palantir’s customer base and larger deal sizes helped it end 2025 with $11.2 billion in remaining deal value (the value of contracts to be fulfilled at the end of a quarter), a threefold jump since the end of 2022. This remarkable growth has translated into a terrific bump in Palantir’s revenue and earnings in recent years.

Data by YCharts.

The AI software platforms market is anticipated to clock a 29% CAGR through 2034. Generating an impressive $237 billion in revenue at the end of the forecast period, Palantir is well placed to sustain its terrific growth rate over the next decade. Moreover, the company is growing faster than the AI software platform market, which can be attributed to its status as a leading player in this industry.

So, investors looking for a company with the potential to capitalize on the growth of the AI software market over the next decade would do well to consider Palantir stock for their portfolios.

Read Next

•By Geoffrey Seiler

Should You Forget Palantir and Buy These 2 Tech Stocks Instead?

•By Adam Spatacco

3 AI Stocks Caught in the Crossfire of the Iran War, and What Smart Investors Should Do in 2026

•By Adria Cimino

Palantir Stock Isn’t Cheap, But It Might Still Be a Bargain

•By Keith Speights

Could Buying Palantir Technologies Today Set You Up for Life?

•By Harsh Chauhan

Why March Could Be a Turning Point for Palantir Stock

•By Danny Vena, CPA

Palantir and Nvidia Join Forces to Tackle This $600 Billion Opportunity

About the Author

Harsh Chauhan is a contributing Motley Fool technology analyst covering semiconductors, consumer electronics, artificial intelligence, and software. Harsh previously worked as a journalist for CCN Markets covering crypto and macroeconomics, a contributor at Capital 10x covering metals, mining, and industrial stocks, and a research associate at Zacks Investment Research. He holds a bachelor’s degree in commerce from St. Xavier’s College in Kolkata, India.

Stocks Mentioned

Palantir Technologies

NASDAQ: PLTR

$150.95

(-1.66%)-$2.55

Taiwan Semiconductor Manufacturing

NYSE: TSM

$338.11

(+0.42%)+$1.40

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Sumber Artikel:

Fool.com